Hello,

I have some issues with the following:

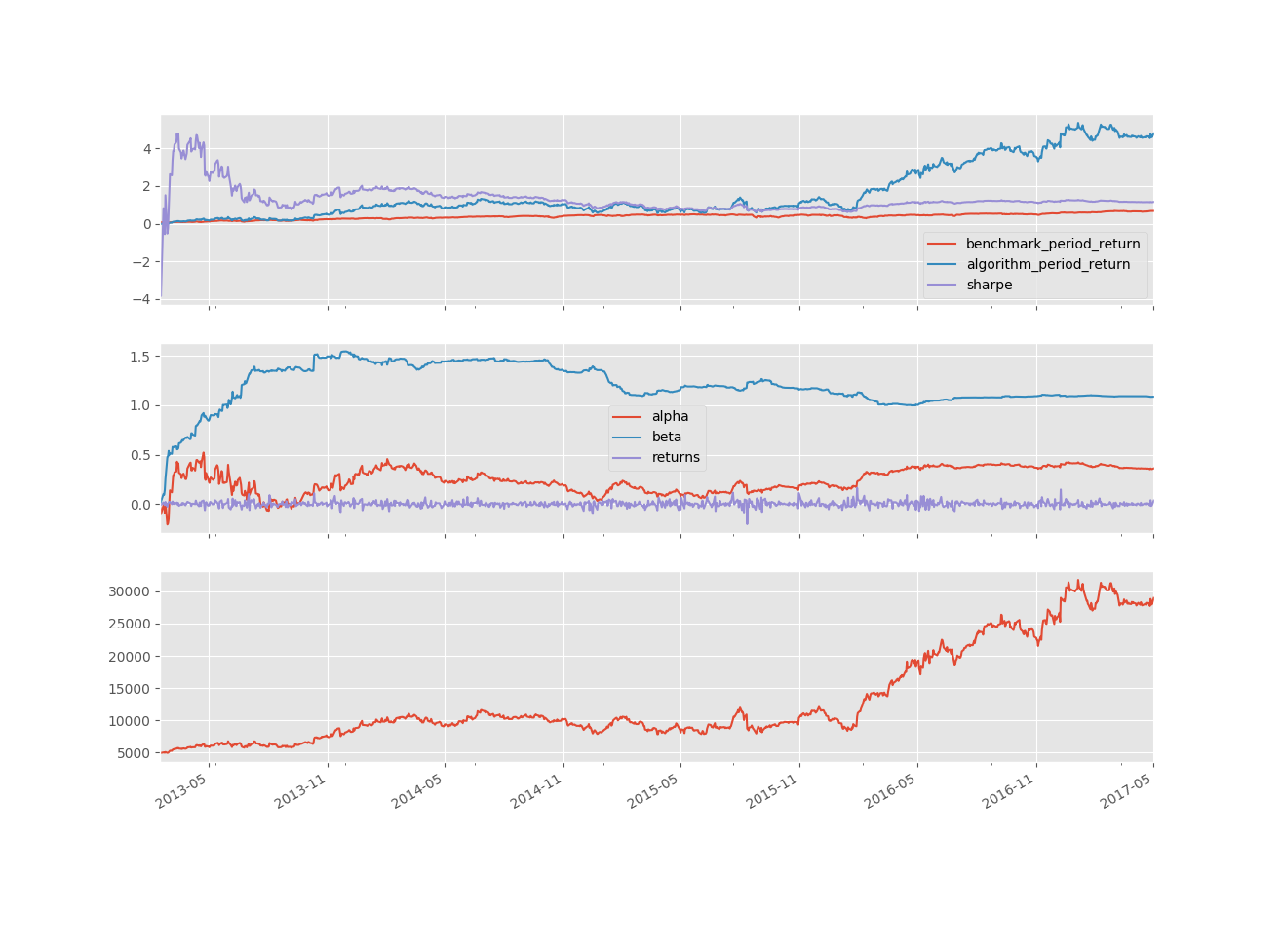

1.) My algorithm using zipline (version 1.1.0) and quantopian-quandl bundle: quantopian-quandl 2017-06-28 05:10:37.356780 gives the following results: https://anon1980.bitbucket.io/Result.png

2.) I ran the exact same algorithm in the IDE and the result is attached. The results are completely different -- all money lost! -- why? what bundle is the IDE using?

3.) I cannot use the research platform and the IDE due to the following reasons:

a.) Memory keeps on running out on the research notebook, by simply adding extra columns.

b.) Not allowed to install packages, for example genetic algorithms, convex optimizers, satisfiability modulo theory optimizers, etc.

c.) Cannot run anything in parallel.

I personally have access to 128 core 256GB shared memory machines, where running the algorithms takes seconds, and never runs out of memory, so I would prefer developing on my machines, rather than Quantopian IDE/research platform.

The only good thing about Quantopian currently is the access to fundamental data via morningstar. Other than that, the infrastructure setup is not meant for quantitative research, and instead for lucky people.

Can you please answer the simple question as to why the results that I get on running on my personal machine vs. the IDE backtest are so different? Can I download the bundle that you are using for backtests from somewhere?

Thanks,

{kind=link}