Maybe someone can code an algo for this notion.

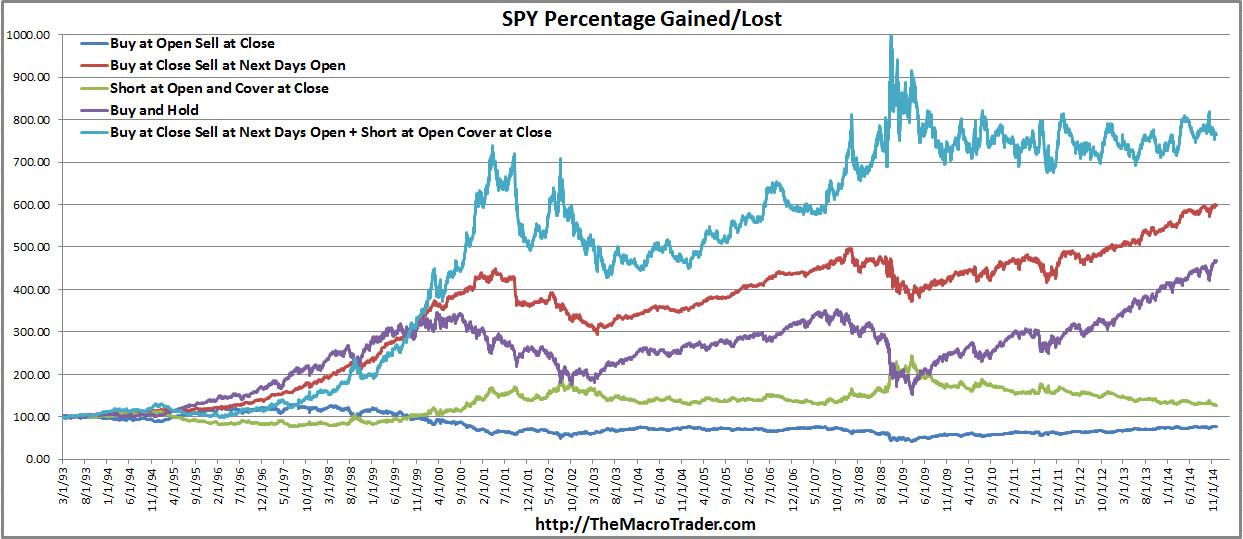

The article (if you can call it that) at InvestmentWatchBlog doesn't have much content, then there's a link to a twitter message with the image below ...

Maybe someone can code an algo for this notion.

The article (if you can call it that) at InvestmentWatchBlog doesn't have much content, then there's a link to a twitter message with the image below ...

Hey Gary,

This is my attempt at an algorithm for the 'long during nights and short during day' strategy.

Commissions and slippage are set to zero.

Note that presently, all Quantopian orders are cancelled at market close under live trading, per the help page:

All open orders are cancelled at end-of-day.

Orders made in the last minute of the trading day will be automatically cancelled.

Presumably, this behavior will change at some point, and overnight orders will be supported.

Note also that the Quantopian backtester will use minutely closing prices for filling orders, so you need a custom slippage model to capture the true daily open.

I did some yahoo data manipulating and come up with the same results as the chart above, pretty interesting. Even in recent years overnight has outperformed intraday, but intraday returns have gotten better.

This test is sorta interesting, it looks at the price change since around mid-day and makes an overnight bet in the opposite direction. I was not expecting it to perform at all, but it did okay. I think these sorts of things are more of a novelty than anything else though because trading fees would eat them alive.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by Quantopian.

In addition, the material offers no opinion with respect to the suitability of any security or specific investment. No information contained herein should be regarded as a suggestion to engage in or refrain from any investment-related course of action as none of Quantopian nor any of its affiliates is undertaking to provide investment advice, act as an adviser to any plan or entity subject to the Employee Retirement Income Security Act of 1974, as amended, individual retirement account or individual retirement annuity, or give advice in a fiduciary capacity with respect to the materials presented herein. If you are an individual retirement or other investor, contact your financial advisor or other fiduciary unrelated to Quantopian about whether any given investment idea, strategy, product or service described herein may be appropriate for your circumstances. All investments involve risk, including loss of principal. Quantopian makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances.